It Doesn't Look or Feel Like a Recession

From time to time, I get asked a question often enough that I use it as a commentary topic. Also, occasionally I have written commentaries on aspects of behavioral finance, one of my personal favorites.

First, the question: “Given the pace (and amount) of rate hikes over the last 18 months and the historic record of rate hikes causing recessions, where is the recession this time? It doesn’t look or feel like a recession.”

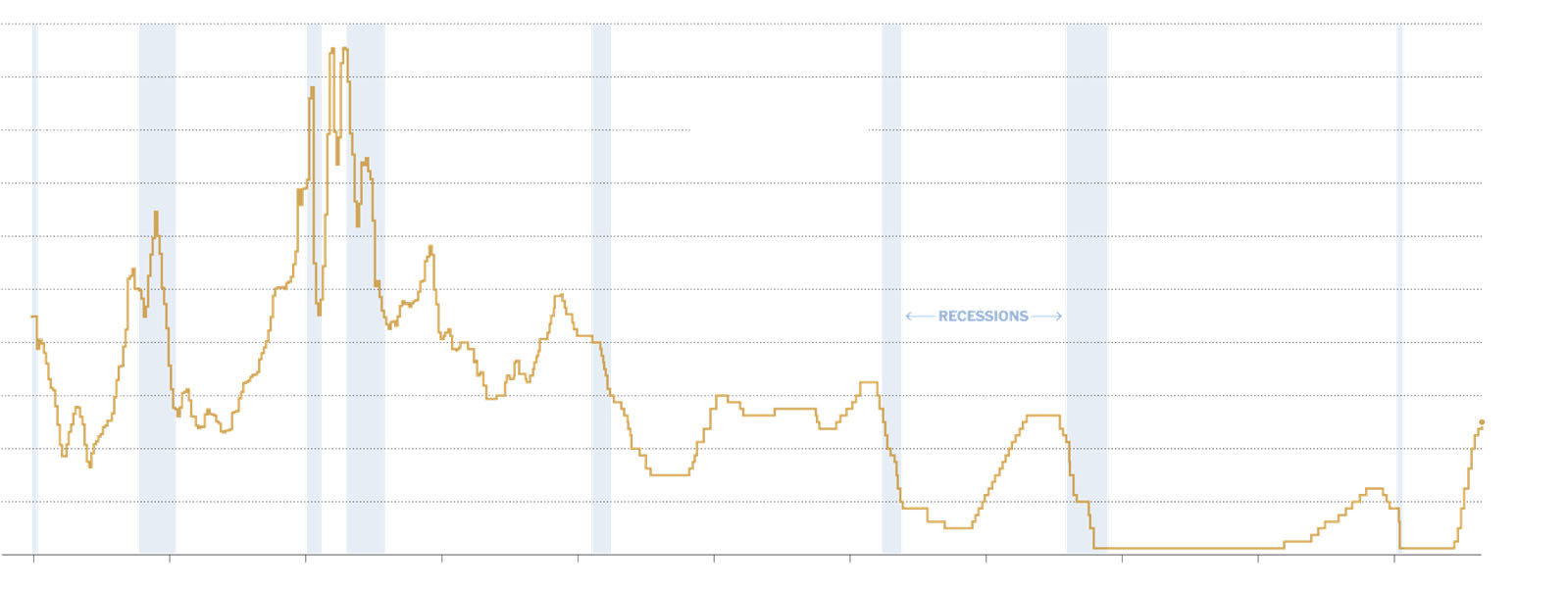

The premise of the question is likely coming from some version of the historical record that the US Central Bank, The Federal Reserve (“the Fed”) has a poor track record of raising rates to fight inflation AND also avoiding a recession. Since 1961, the Fed has avoided a recession just once (1994) in the nine rate increase cycles. Mathematically, the odds of a recession are high, and likely justify a conservative approach to spending, borrowing and financial planning.

However, each market cycle is uniquely its own. And taking drastic steps to adjust investment allocations can just as often create problems rather than avoid risks. The anticipation of future recessions or stock market declines can often result in missed opportunities and continued market cycle growth. We are now 18 months into the current rate hike cycle and there is still very little evidence to support recessionary concerns. Unemployment remains very low, consumers are still spending, and the official government consumer price index (“CPI”) measure of inflation is dropping toward the Fed’s target rate suggesting that the Fed may be able to slow rate hikes or pause them altogether.

One unique aspect of the current economic cycle is the post-pandemic mindset toward spending. A behavioral observation, and one that gets far less press than the headlines of political upheaval, bank runs or the price of gasoline is the phenomenon called “retail therapy.” After experiencing loss of loved ones or feeling isolated and alone or having a near-death experience, there is a propensity to spend or enjoy or splurge a bit. You may have also heard it called “revenge vacationing” or “grief shopping.” In the time since Covid-19pandemic, spending on trips and luxury items and other goods has been a coping mechanism, a way to make up for lost time (in lock downs) and a way to take back some control. Additionally, some would-be home buyers have decided that rates have pushed their home ownership dream out of reach and have decided to spend savings otherwise earmarked for down payments.

Everyone grieves in their own way and for their own reasons. Some might want to feel “whole” again and others want to regain control over their lives. Some will go on trips, some will remodel their house, some will buy luxury items and pamper themselves, buy a new watch, a new car, new clothes.

US households have spent $2.1 trillion in excess savings since the pandemic. Credit card balances rose by over $45 billion last quarter and have now crossed over $1 trillion in cumulative credit card debt which commonly carry 20%+ interest rates.

The US government stimulus helped provide much of the spending power that the pent-up (literally) population was ready to use. And consumers appear to be consoling themselves, in part, through spending. Regaining a sense of control is a basic human need, and for many, spending money on items and trips and experiences can help. If this behavioral response to Covid -19 pandemic is part of the reason why consumption has remained stronger than anticipated, then one might ask how much longer the current level of spending can continue. The holidays are right around the corner, and employment has remained strong, so perhaps consumer spending will remain robust at least through the end of 2023.

In investing, we must always leave room for the unknowable, the black swan, the unexpected or unimaginable. The proverbial “x” factor. In previous rate hike cycles, unique events unfolded that looked or acted differently than previously observable cycles. We cannot simply watch rates go higher and know for certain a recession will follow. We cannot know exactly how it will impact our own lives. In previous cycles, major disruptive headliner events have included a savings and loan crisis, a tech crash, a US housing crash, bank failures, currency crisis, and more. What we can know is that rising interest rates put pressure on a leveraged system. Rising interest rates mean higher debt costs, lower corporate margins (if price increases cannot be pushed through to the end user), higher refinancing costs, and (usually) reductions in asset price valuations. When asset values decline and debt borrowing costs rise, it creates a squeezing effect that can break things. If all goes well, the rising interest rates can reduce inflation by slowing down economic price pressures, but often these rate hikes come at a cost of breaking things like banks, currencies, corporations, stocks, and real estate projects which can lead to layoffs, falling consumer sentiment (which leads to less spending and gloomy outlook), market crashes, and other follow-on impacts. As history suggests, it is quite difficult to get the rate hikes “just right” and defeat inflation while also maintaining a growing economic cycle.

Securities markets can be fickle and are often completely out of sync with human realities and emotions. The current low unemployment rate is great for those with jobs, and for consumer spending, but also may be part of the reason inflation is so stubborn. The securities markets may perceive some layoffs and lost jobs as a “good” thing from an inflationary perspective, but then later perceive too many job losses and “bad” and fear a recession. Right now, the common knowledge of the markets might be summed up as “we need some bad news/events to cause the Fed to pause its rate hikes, but not so bad that it causes stock or real estate prices to fall.” I would observe that most consumers not only need their jobs to continue but also be able to anticipate higher wages to offset higher living costs.

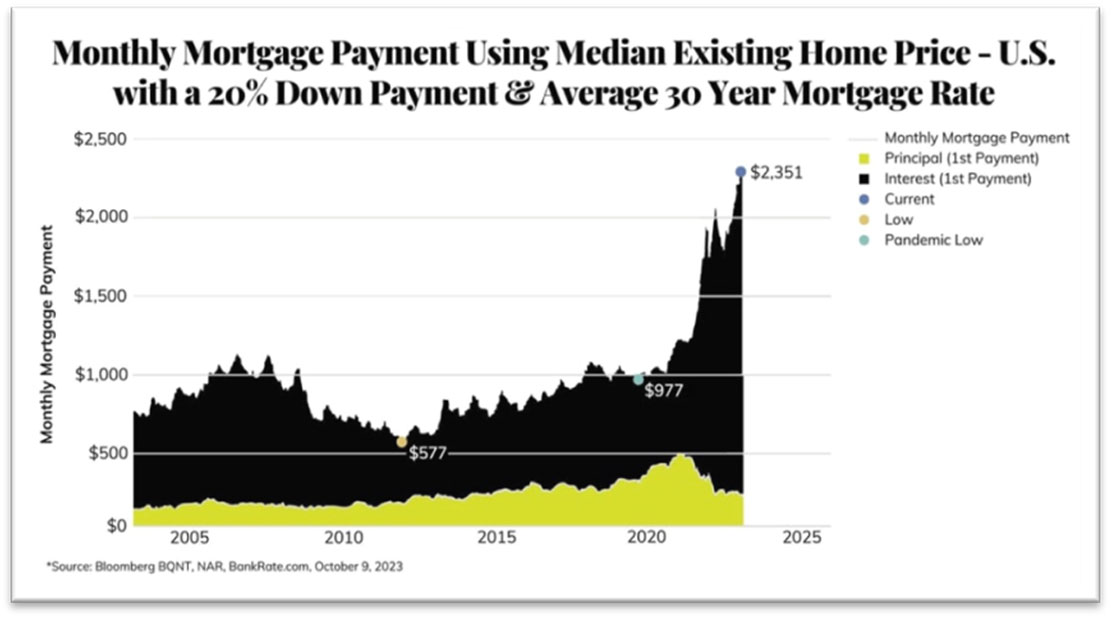

Historically speaking, stocks are at a level we might term “over-valued” given the current interest rate on bonds and price-to-earnings multiples on stocks. The Wilshire 5000 stock index is nearly 1.6x larger than the US Gross National Product (GNP), which is down from its extreme levels but still high when compared to its historic range. Same goes for real estate. While an individual property is unique and must be judged on its own merits and not compared solely to an aggregate index, the average home price is nearly 7x the level of median income and well above its historic average. Commercial real estate is experiencing far more contraction than residential real estate and office space is a downright terrible sector.

When interest rates hovered near zero during the 2010’s, a very real risk was holding cash and losing the purchasing power relative to inflation. Cash was almost forced into stocks and real estate and growth ventures. Interest rates were negligible. With asset prices at somewhat elevated levels today however, and the current rate of “safe” interest now between 5-5.5% in money markets and CD's, and with mortgage rates moving toward 8.0%, investors are finding it easier to wait and see what may happen in the current economic cycle.

There are stocks, and even some industries, within the US economy priced at buyable levels. As always “the market” is just an average of the total components, some are expensive and overvalued and others offer a good long-term opportunity. This is also true in real estate. Indexes and market can provide an overall summary on valuation, but we can still search out quality ideas that make sense today.

Next quarter we will look at 2024, an election year. Over the past 100 years, election years have resulted in lower-than-normal stock market returns. Current asset price levels, economic cycle timing and an election year all suggest a tilt toward safety may be appropriate for most investors. Our recommendation to “tilt” toward conservatism remains the same. For most people a “tilt” is a re-allocation of 10-15% of their normal growth holdings and to earn safer returns of 5.0-6.0% while waiting out the current economic environment. For example, if the long-term investment policy of a portfolio calls for 60% in growth assets, then a 10-15% underweight from normal policy would be 51% to 54% in growth holdings.

By allocating a lower percentage to growth holdings while values are relatively high, most investors will more easily respond correctly to a future drop in asset prices and add to growth, even while headlines are negative.

In conclusion, while grief shopping and revenge travel may be helping delay a recession in an economy facing headwinds such as high inflation and rising interest rates, it is important to note that these behaviors are not sustainable in the long run. Eventually, consumers will run out of money or will no longer feel the need to engage in these behaviors. Similarly, while government intervention may be helping delay a recession in the short term, it is important to note that these measures are not sustainable in the long run. Eventually, governments will need to reduce their spending or risk running up large deficits.

*The foregoing content reflects the opinions of Van Hulzen Asset Management DBA "Van Hulzen Financial Advisors" and is subject to change at any time without notice. For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is based on third party data and may become outdated or otherwise superseded without notice. Third party information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Mentions of specific securities should not be deemed as a recommendation. Indices are not available for direct investment. Their performance does not reflect the expenses associated with the management of an actual portfolio nor do indices represent results of actual trading. Information from sources deemed reliable, but its accuracy cannot be guaranteed. Performance is historical and does not guarantee future results. All investments involve risk, including loss of principal.