Q2 2025 Market Commentary

A World in Transition – Slowing, But Not Sinking

As we move into the second half of 2025, the global economy and financial markets are reshaped by profound structural changes. The era of stability and predictable policy is giving way to one defined by fragmentation, transformation, and the erosion of traditional economic anchors. Yet, despite these seismic shifts, the economy has shown remarkable resilience throughout the first half of the year. Growth is moderating rather than collapsing, with structural changes unfolding unevenly across regions and industries. In this evolving environment, tactical flexibility, thematic investment focus, and active risk management are essential.

Fragmentation and the Erosion of Macro Anchors

The global financial system is undergoing a significant shift. Historically reliable macro anchors such as steady growth, low inflation, inexpensive credit, and globalization are no longer assured. More governments are now placing a higher priority on national security and sovereignty over economic efficiency, prompting shifts in global alliances and economic structures. This reordering is driving changes in trade policy, industrial strategy, and fueling rising geopolitical tensions. In our view, these are structural, not cyclical developments, which expand the range of possible outcomes and increase risk premiums across asset classes. The resulting environment is fragile. Unwinding decades-old trade and capital structures is a complex, time-consuming process. Supply chains can't be reimagined overnight without significant disruption. Companies face challenges in sourcing products and materials, which explains the rapid introduction of tariff carve-outs (such as exemptions for rare earth minerals and electronics) and repeated extensions of trade deadlines¹. In the short term, these carve-outs and extensions have softened the impact on consumer spending and corporate profit margins, allowing markets to reach all-time highs by the end of Q2. However, much remains uncertain, and the effects will vary across sectors and industries.

Moderating Growth, Not Collapse

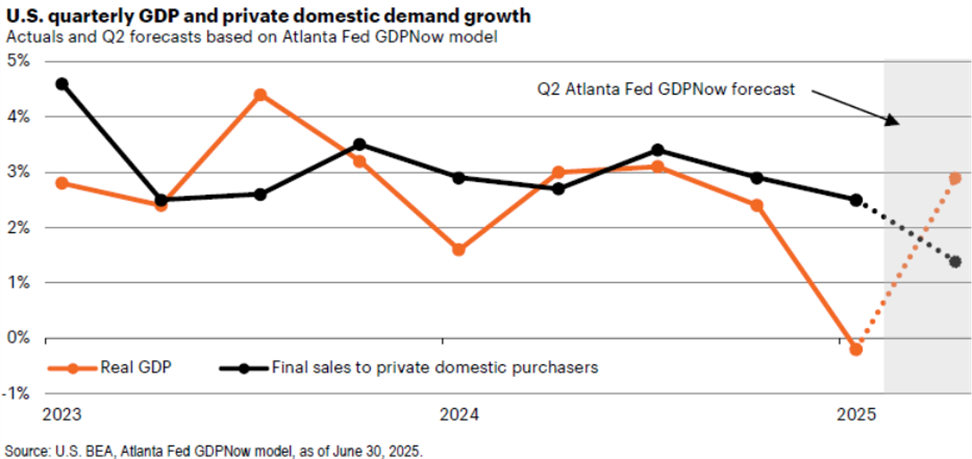

Recent economic data from Q2 highlights a resilient U.S. economy, albeit with signs of deceleration. While headline GDP growth dipped in Q1, largely due to a surge in imports ahead of tariff increases², final sales to private domestic purchasers (a more stable measure of demand) rose by 2.5%, with Q2 forecasts around 1.6%³. Consumer spending, which accounts for roughly two-thirds of U.S. GDP, continues to be the main driver of growth, supported by solid wage increases (4–5% year-over-year) ⁴ and a recovery in personal savings.

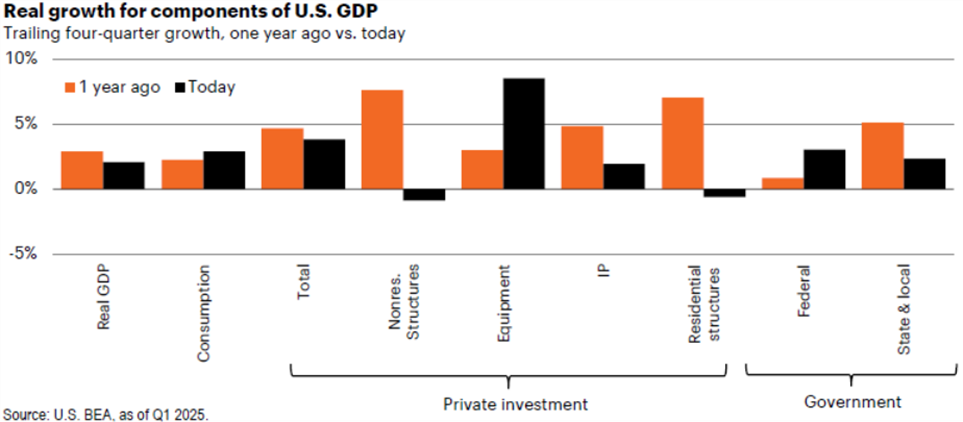

The AI capital expenditure boom continues its impressive run⁵, but corporate investment, government spending, and residential investment are all showing signs of slowing. Many corporate management teams are taking a cautious approach, delaying capital expenditure until there is greater clarity on tariffs. This places additional importance, and risk, on consumer spending as the backbone of the economy.

Key Risks We’re Watching

Although our base case sees only moderate slowing, we are closely monitoring several key downside risks:

• Tariff Spillovers: Companies can currently pass through only about two-thirds of additional tariff-related costs, raising concerns about margin compression and earnings vulnerability.

• Geopolitical Volatility: Flashpoints in the Middle East, Eastern Europe, and U.S.-China relations continue to elevate global risk, threatening sentiment and capital flows.

• Labor Market Softening: Stricter immigration measures could slow labor supply growth, causing bottlenecks in industries like construction and hospitality, and driving up unit labor costs.

• Housing Inflection Point: Existing home inventories are rising, especially in the Sun Belt, and downward price pressure may soon follow, potentially impacting investment and consumer wealth.

• Inflation Expectations: While inflation is currently under control, expectations remain volatile. If consumers start to anticipate persistent inflation, the Fed may be forced to tighten policy further.

Positioning for What Lies Ahead

With traditional macro anchors in flux, risk management is more vital than ever. A wider range of potential outcomes means that diversification and an emphasis on quality should be top priorities.

• Equities: In a turbulent, fragmented landscape, companies have new challenges that could pressure profit margins. We favor high-quality businesses with consistent returns above their cost of capital, and we remain focused on the transformative opportunities in AI.

• Fixed Income: Monitor duration risk carefully as term premium (the additional yield for holding longer-term bonds) remains elevated.

Final Thoughts

We believe we are living through a fundamental and dynamic transformation of the global macro regime. The transition is sure to have pitfalls and unexpected consequences. Despite these challenges, this new era also brings fresh opportunities. Tactical flexibility, structural awareness, and active risk management will be essential tools for navigating the years ahead.

Thank you for your continued trust. We remain committed to providing you with clear guidance and timely service as we move forward together.

Footnotes

1. Reuters, U.S. rare earth pricing system is poised to challenge China’s dominance, July 2025. Link

2. U.S. Bureau of Economic Analysis, Gross Domestic Product, First Quarter 2025 (Second Estimate), May 29, 2025. PDF available on the Bureau's website

3. Federal Reserve Bank of St. Louis, Real Final Sales to Private Domestic Purchasers. Link

4. U.S. Bureau of Labor Statistics, Employment Cost Index Summary, Q2 2025. Link

5. Bond Capital, Trends – Artificial Intelligence, May 2025. PDF available at Bond Capital website.

*The foregoing content reflects the opinions of Van Hulzen Asset Management DBA "Van Hulzen Financial Advisors" and is subject to change at any time without notice. Content provided herein is for informational purposes only and should not be used or construed as investment advice or a recommendation regarding the purchase or sale of any security. There is no guarantee that the statements, opinions or forecasts provided herein will prove to be correct. Past performance may not be indicative of future results. Indices are not available for direct investment. Any investor who attempts to mimic the performance of an index would incur fees and expenses which would reduce returns. Securities investing involves risk, including the potential for loss of principal. There is no assurance that any invest-ment plan or strategy will be successful.

Van Hulzen Asset Management is an investment advisory firm registered with the Securities and Exchange Commission (“SEC”). SEC registration does not imply a certain level of skill and or expertise. Van Hulzen Asset Management does not provide tax advice, please consult your tax professional for any specific tax related questions.