Q3 2025 Market Commentary

The History of Ledgers: How Trust Has Evolved in Finance

For thousands of years, merchants recorded their day’s trade in a single ledger—one column for money in, one for money out. Single-entry accounting was simple but fragile. If a merchant misplaced a page or fudged a number, no one would know. Trust rested entirely on the individual’s honesty and diligence.

In the late 1200s to mid-1300s, Italian merchants adopted a new system: double-entry accounting. Every transaction now appeared twice—a debit in one account and a credit in another. If the books didn’t balance, something was wrong. This innovation transformed trade, enabling audits and building trust.

In the modern era, people stopped recording transactions in physical ledgers and began recording them into analog computers. Corporate financial statements, bank ledgers, and clearinghouses all maintained centralized databases built on the same double-entry accounting system developed centuries ago. While these databases increased transaction speed and reduced errors, they also concentrated trust and fraud risk within a few central institutions. This created single points of failure, making centralized databases attractive targets for hackers and large-scale data breaches.

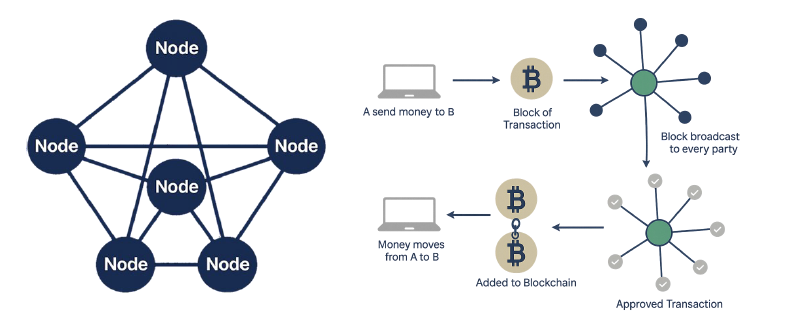

Now, picture TODAY. Instead of centralized ledgers or databases, imagine millions of ledgers —verified computers called nodes— spread across the globe, all checking each other’s work. This is the concept behind blockchain technology—a distributed system where every transaction is verified by consensus and locked in place with cryptography eliminating single points of failure. Think of it as triple-entry accounting:

• Debit

• Credit

• Cryptographic receipt notarized across all ledgers

For the first time, there is a verified system that doesn’t depend on a single person, bank, or server, but rather the decentralized global network itself. Reducing the risk of large-scale hacks and undetected fraud compared to traditional centralized systems.

Adapted from “Blockchain Technology — Introduction,” GeeksforGeeks"

DeFi—How Blockchain Technology is Changing Finance

Modern finance relied on intermediaries: banks, brokers, clearinghouses, payment networks, and courts. These institutions exist because we need trust. When we wire money, we trust the bank. When we buy stock, we trust the exchange and the regulator. When there’s a conflict, we trust the judicial system.

Decentralized Finance (DeFi) asks: What if trust could be replaced by transparent, auditable code? Instead of legal contracts en-forced by courts, we have self-executing digital agreements—smart contracts—written directly into lines of code on a blockchain. These contracts trigger automatically when predetermined conditions are met, reducing the need for traditional intermediaries.

Consider a vending machine: the code (the smart contract) is programmed to dispense a snack (the outcome) once the correct amount of money (the condition) is inserted. The machine won’t release the snack until all terms are met, and will return the money if they aren’t.

Now imagine a large grocery store purchasing food from many farms with if/then smart contracts built on-chain—if a delivery is confirmed by the buyer’s system, then payment is automatically released. This not only makes transactions more efficient but also improves supply chain transparency, allowing for quicker tracing of product origins in case of recalls.

This is the premise of DeFi, where the “rules” of financial interactions are written directly into transparent, traceable, and an im-mutable code confirmed by millions of decentralized computers, making processes more efficient.

How Smart Contracts Work:

· Code substitutes for law: The agreement’s terms are translated into computer code and stored on a blockchain.

· Automatic execution: When the conditions in the code are fulfilled, the contract automatically executes the agreed-upon actions.

· Decentralized and secure: Running on a blockchain, smart contracts are tamper-proof, secure, and transparent.

· Reducing intermediaries: Automation reduces the need for third parties, minimizing costs, fraud, and delays.

The Road Ahead

If the internet decentralized information, and social media decentralized communication, then DeFi is decentralizing value itself.

Over the past few decades, we’ve witnessed a series of profound technological shifts that have fundamentally changed how we interact with the world—and with each other. Each wave of innovation has brought greater decentralization, empowering individuals, and reshaping entire industries.

First, the internet decentralized information. Where once knowledge was controlled by centralized entities like libraries, publishers, and media companies, the internet broke down those barriers. Suddenly, anyone could publish and access information globally, democratizing knowledge and making it available to all.

Next, social media decentralized communication. In the past, large-scale communication was dominated by broadcasters and newspapers. Social media platforms gave individuals the ability to communicate directly with vast audiences, bypassing traditional gatekeepers and amplifying every voice.

TODAY, DeFi is decentralizing value itself. Traditional finance has long relied on centralized institutions—banks, payment processors, and governments—to store, transfer, and manage money and assets. DeFi leverages blockchain technology and smart con-tracts to enable people to exchange, lend, borrow, and invest without intermediaries. It’s removing the need for centralized trust and replacing it with transparent, decentralized protocols.

In short:

· The internet democratized knowledge.

· Social media democratized voice.

· DeFi is democratizing money and financial power.

This matters because it challenges centuries of financial architecture by turning money into programmable code and invites the world to build new forms of credit, ownership, and trust. We believe the next decade will not be a battle between “crypto vs. banks,” but rather a fusion—a layered, programmable, global financial network where the rules of money are written in code rather than legal contracts.

We are seeing this unfold in real time, with major corporations and financial institutions experimenting with blockchain technology for specific use cases. For example:

· AXA: Piloted blockchain-based insurance products, where claims are automatically paid out via smart contracts when certain conditions are met.

· JPMorgan Chase: In 2023, launched a pilot program with several Indian banks to settle U.S. dollar transactions instantly, reducing costs and improving efficiency.

· Visa & Mastercard: Both are experimenting with blockchain for cross-border payments, aiming to make international money transfers faster and less expensive.

· Walmart: Uses blockchain technology, in partnership with IBM, to track food products from farm to store, improving supply chain transparency and food safety.

These examples show that blockchain and DeFi are not just theoretical concepts, they’re being actively used by some of the world’s largest and most trusted companies to improve efficiency, transparency, and security across industries.

In Closing

We live in a time of several major technological shifts, including the rise of AI, blockchain, and decentralized finance. These changes can bring both opportunity and uncertainty. At Van Hulzen Financial Advisors, we are dedicated to staying informed about these trends and evaluating how they may impact markets and your portfolio. By remaining adaptable and forward-thinking, we aim to help you navigate these changes with clarity and confidence.

We remain focused on both the opportunities and risks that come with innovation, ensuring your portfolio is positioned to bene-fit from progress while maintaining a strong emphasis on prudent risk management.

*The foregoing content reflects the opinions of Van Hulzen Asset Management DBA "Van Hulzen Financial Advisors" and is subject to change at any time without notice. Content provided herein is for information-al purposes only and should not be used or construed as investment advice or a recommendation regarding the purchase or sale of any security. There is no guarantee that the statements, opinions or forecasts provided herein will prove to be correct. Past performance may not be indicative of future results. Indices are not available for direct investment. Any investor who attempts to mimic the performance of an index would incur fees and expenses which would reduce returns. Securities investing involves risk, including the potential for loss of principal. There is no assurance that any investment plan or strategy will be successful. Van Hulzen Asset Management is an investment advisory firm registered with the Securities and Exchange Commission (“SEC”). SEC registration does not imply a certain level of skill and or expertise. Van Hulzen Asset Management does not provide tax advice, please consult your tax professional for any specific tax related questions.