The Cost of Waiting When Planning for Your Child's Future

When it comes to planning for a child with special needs, many families tuck money into a savings account or a CD and think, “it’s safe.”

But what if I told you that kind of safety is actually a guaranteed loss?

Here’s the truth: parking cash over the long term doesn’t protect your money—it slowly eats it away. Thanks to inflation, that “safe” $100,000 may be worth half its value in just a couple decades. That’s not preserving capital. That’s quietly losing ground.

Ironically, the move people fear most—investing—is what historically protects purchasing power over time.

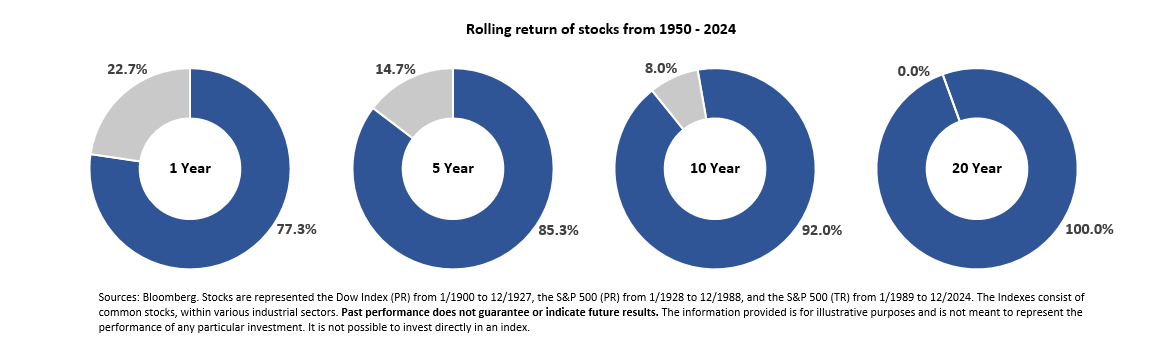

Markets feel risky because they move. But when you zoom out over 5, 10, or 20 years, that movement tends to trend upward, not downward. The longer your timeline, the lower your actual risk becomes.

This chart above shows that the longer money stays invested in the market, the more likely it is to grow. Over time, the odds of a positive return have been overwhelmingly in your favor—unlike cash, which quietly loses value to inflation year after year.

So the real question isn’t “Should I invest?”—it’s, “How long do I have to invest before I need the money?”

It's Not All or Nothing

Let’s clear up a common misconception: financial planning or investing isn’t only about picking stocks or going “all in” on the market. It’s about aligning your dollars with your time horizon, or matching your assets to your liabilities.

That goes for the money you’ve set aside for your child—and for your own retirement.

If you’ll need those dollars in the next 12–24 months, sure—cash or short-term bonds make sense.

But if you’re thinking long-term—college in 10 years, or care expenses decades from now—then staying in cash means locking in a loss.

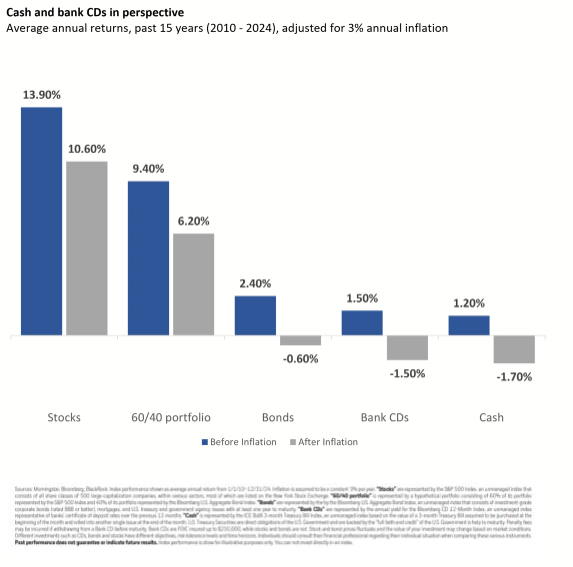

Here’s what the average annualized return for the last 15 years looked like, adjusted for 3% inflation:

So while it might feel safer to sit on the sidelines, it’s actually costing you every year. That erosion compounds quietly—and dangerously.

Now imagine this playing out not just for your child’s future, but your own.

The same math applies.

A healthy financial plan doesn’t avoid risk—it manages it through diversification, time, and purpose.

If you’ve got years before that money will be used, your greatest risk may be doing nothing.

Let’s Talk

If you’re sitting on a chunk of cash set aside for your child’s future and wondering what to do with it, let’s talk.

Together, we can:

- Clarify your goals

- Consider your time horizon

- Build a growth strategy that fits your comfort level

The safest plan isn’t about avoiding risk—It’s about understanding it, and preparing with purpose.

*The foregoing content reflects the opinions of Van Hulzen Asset Management DBA "Van Hulzen Financial Advisors" and is subject to change at any time without notice. Content provided herein is for informational purposes only and should not be used or construed as investment advice or a recommendation regarding the purchase or sale of any security. There is no guarantee that the statements, opinions or forecasts provided herein will prove to be correct. Past performance may not be indicative of future results. Indices are not available for direct investment. Any investor who attempts to mimic the performance of an index would incur fees and expenses which would reduce returns. Securities investing involves risk, including the potential for loss of principal. There is no assurance that any investment plan or strategy will be successful.